Home prices continue to rise, and the big question is how long they will continue to rise, taking into account current market dynamics. According to a pessimistic view, the spiral will continue as long as the housing deficit persists, the result of a misalignment between the size of real estate and the needs of families who aspire to have a roof over their heads, including the hundreds of thousands of young people who cannot emancipate themselves.

This deficit, estimated at around half a million homes, will persist at least until the end of the decade, even in the (ill-advised, depending on how you look at it) hypothesis of a sustained recovery in construction activity. This means that the cycle of rising house prices will not end until 2030.

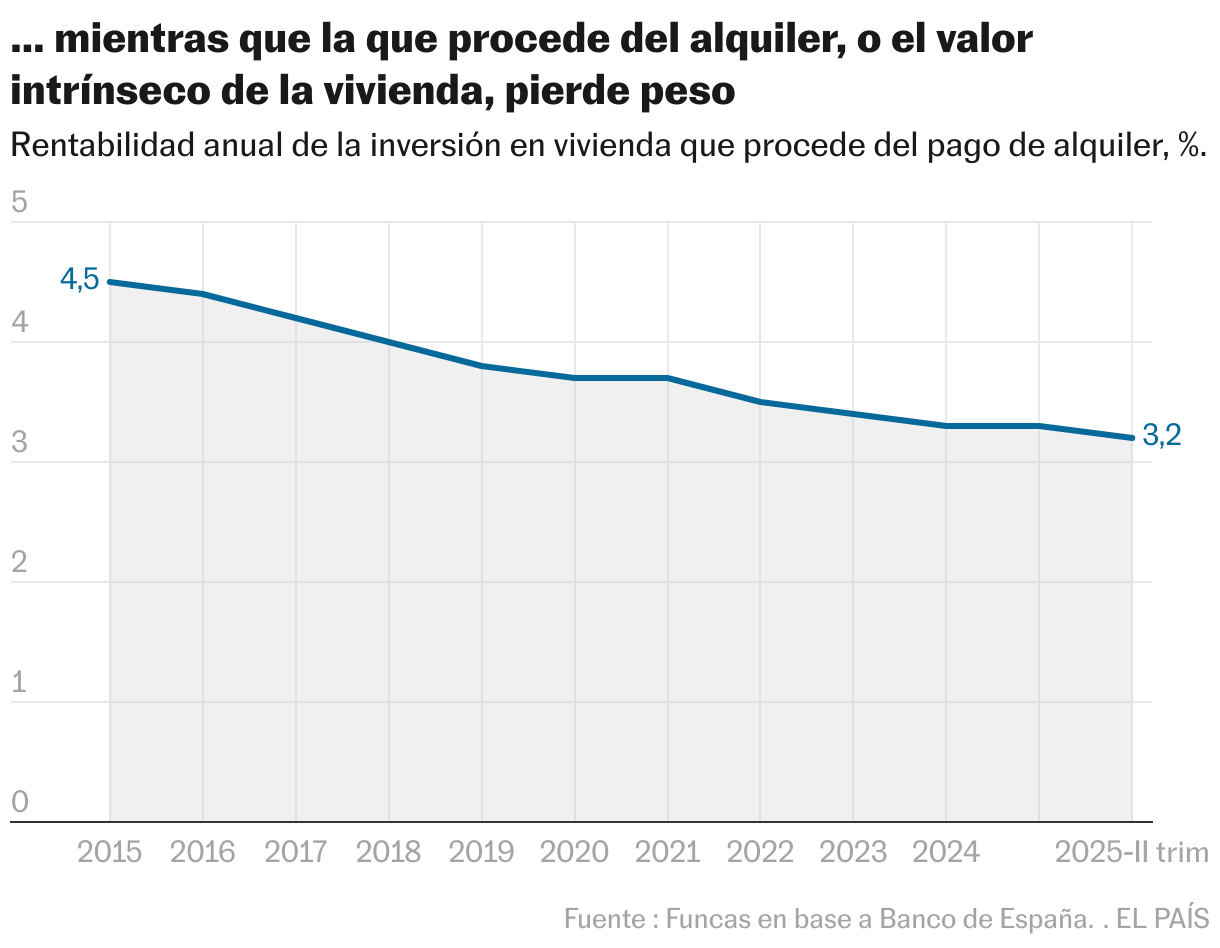

But housing is not like bread, which rises almost instantly when flour becomes scarce or consumption skyrockets, and vice versa. Unlike other assets, a home is an asset that can be exchanged multiple times over its long useful life. Their prices, therefore, do not only depend on current market conditions: expectations, i.e. buyers’ anticipation of future prices, also influence. Therefore, the prospect of a strong capital gain constitutes a powerful incentive to purchase, even when solvent demand begins to run low, as is currently the case in some territories.

Therefore, the price can moderate, even when the housing deficit persists. Only in this way can we explain that in France, where there is also a lack of residential supply, prices have fallen by 14% in real terms compared to the highs reached at the end of 2022. In Germany and Sweden, where a real estate deficit also persists, the correction was even more marked (in the order of 20%), due to the same effect of the change in expectations.

In Spain some signs point to an imminent turning point. Buying a house costs on average 7.7 times a family’s annual disposable income, which is one year more than the same operation cost before the pandemic. According to this indicator we would find ourselves at values close to those observed in the period before the real estate bubble, even if on this occasion the dynamic comes from the market itself and not from credit.

Sales volume has slowed, especially in the most stressed areas such as Madrid, Barcelona and some coastal regions. It is likely that the group of families who are buying a home for the first time will be increasingly minority, given the enormous volume of savings needed to buy a house without having previously sold another. Buying in the center of our main cities costs more than in Germany or Italy, and a little less than in France, all countries with a higher per capita income than in these parts. And rent follows a similar path as leases expire.

The change in trend is also noticeable in the new homes segment, which is the most expensive, and also the most responsive to the increase in supply. This is precisely the priority: to accelerate construction, especially affordable construction.

The solutions are well known, as are the brakes, in the case, for example, of the release of building land. But technology advances and new building materials have been developed, making it easier to reduce construction lead times and production costs. The financial engineering of these techniques, which are both innovative and initial capital intensive on the part of the promoters, needs to be adapted. All this would pave the way for a deflation of expectations and a greater balance in the market of such an essential good.

Prices

Over the past three years, the real estate price index prepared by the INE has increased by almost 25%, or 11% discounting the effect of inflation (compared to the first half of this year with the same period of 2022). Over the same period, the price fell by 7% in real terms across the eurozone as a whole, a trend shared by Europe’s large economies. Among the exceptions, the case of Portugal stands out, with an increase of 21% more than double that of Spain.

Raymond Torres is director of Funcas Coyuntura. In X: @RaymondTorres_