The Spanish economy continues to resist the international storm, as well as the reformist paralysis that comes with it sudoku Spanish politician, and the feeling of inertia that has taken over the European Union in the face of Mario Draghi’s complaints. Despite the entry into force of tariffs imposed by the Donald Trump administration, Spain’s GDP grew 2.8% in the third quarter, compared to 1.3% for the Eurozone as a whole, according to information released this week.

Growth, however, is less balanced, prefiguring a change in model with significant implications for economic policy. Of the two engines of the economy, the internal and the external one, only the first is pulling, while the second is accumulating worrying signs of exhaustion.

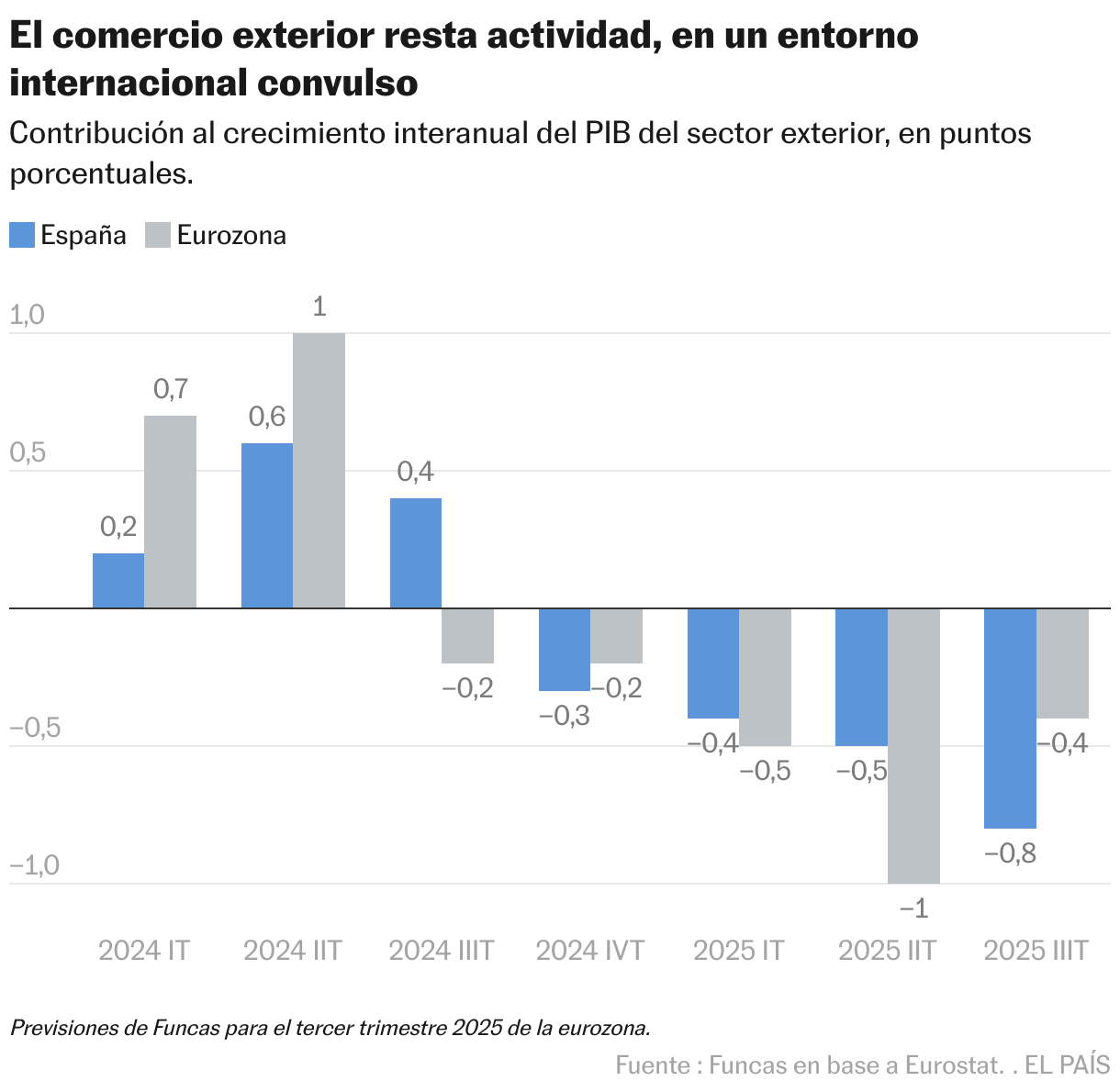

During the previous three-year period, exports had increased more rapidly than imports, both in terms of current prices and volume, so that the foreign sector played a leading role in the expansionary cycle, also resulting in significant surpluses in foreign currencies. In recent quarters the trend has clearly reversed as, despite the stability of exports, imports have recorded a surprising acceleration. So far this year, foreign sales have increased by 3.6%, which is close to the same period last year, while imports have increased by 5.8%, double that of last year (at constant prices).

In short, the foreign sector no longer contributes to the business, but rather takes away from it. And the latest data suggests that this situation is expected to persist. On the one hand, there is a decline in exports, in particular to the United States, a logical consequence of the tariff war; and a moderation in the entry of foreign tourists, in a context of saturation of some destinations and stagnation in the purchasing power of visitors. Imports, however, continue to grow at a high rate, particularly those from the United States and China.

The push, therefore, will only come from our forces, among which family consumption stands out, the variable that has contributed most to the GDP growth recorded so far this year, followed by investments. Underlying this achievement is, firstly, the creation of jobs, encouraged by the incorporation of immigrants, and secondly the accelerated implementation of European funds, as the program enters its final phase. Current indicators also consolidate the recovery in residential investments, a factor with greater potential for persistence compared to Next Generation resources.

In any case, we are faced with a growth model based on the abundance of domestic spending, the reflection of which can already be read in the consumer price index. Inflation is around 3%, compared to 2% in the Eurozone, due to the pressure of consumer spending on prices in service sectors that operate sheltered from international competition. The gap with Europe in terms of underlying inflation is also verifiable, i.e. excluding energy and fresh food. If this continues, the differential will filter into production costs, reducing the extra competitiveness that, even today, provides strength to the Spanish economy.

In other times, the current increase in inflation in a context of strong expansion in domestic spending would have led to a slight increase in interest rates. The ECB, however, will not take this step as it has to take into account the general situation, which is much less favorable than ours. Macroeconomic management, therefore, must be based on fiscal policy, and more specifically on the containment of current spending by administrations. The dilemma is how to achieve this goal and at the same time meet the social demands resulting from strong population growth.

Employment

According to national accounts data, in the third quarter the number of employed people grew by 0.7%, while the total hours worked grew by 1%, so there was a slight recovery in the number of hours worked per employee. Hourly productivity recorded a decline of 0.4% in the quarter, despite the cumulative increase of 0.9% for the year. Compared to the pre-pandemic period, productivity per hour worked grew at an average annual rate of 0.6%.