The food industry enters the final stretch of an abnormally stable fiscal year 2025. At least in comparison with the situation of the previous three years, marked first by the inflationary shock unleashed following the Russian invasion of Ukraine, and which caused an unusual increase in costs for businesses; and then, for the management that companies had to do with their economic accounts. They faced a key decision: whether or not to fully pass on these increases to sales prices.

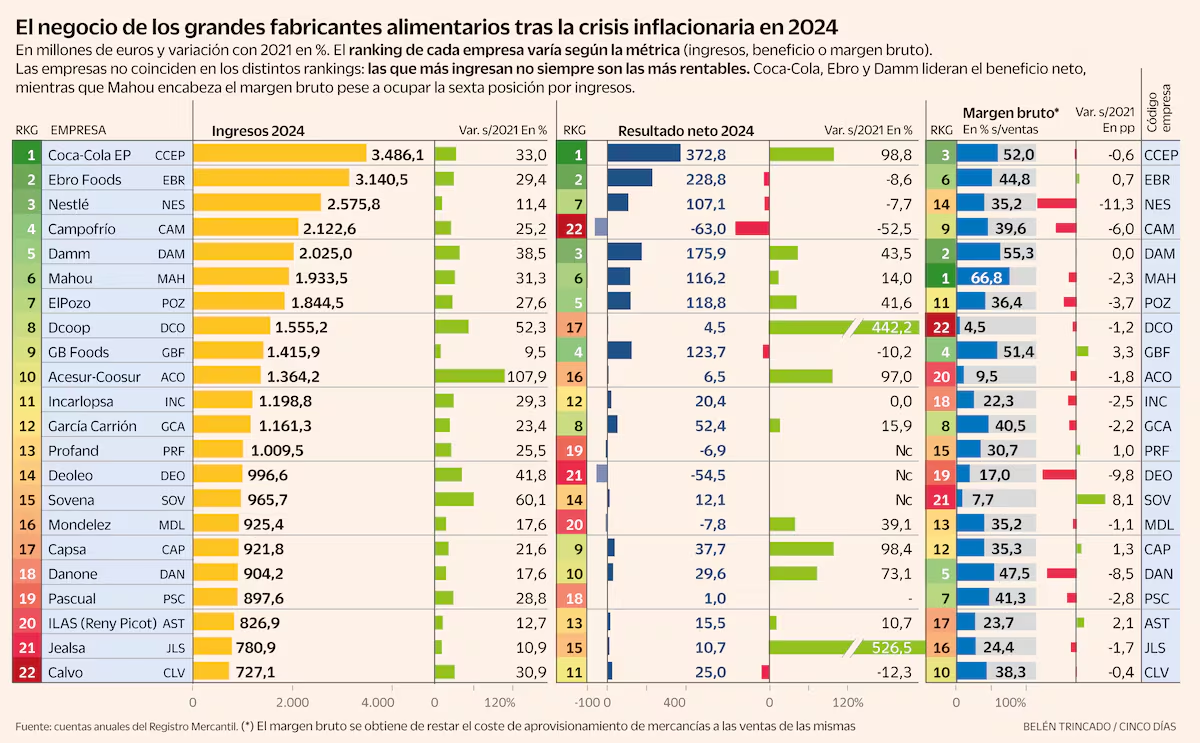

The analysis of the balance sheets of 22 large Spanish food producers between 2021, the last before the great cost crisis, and 2024, the first of a more stable inflationary situation, allows us to draw the first conclusions. The first: aggregate income grew in that period by 29%, while procurement costs, what you pay for raw materials, grew by 35.5%. Therefore, not all of this increase was passed on to the price.

Despite this, most have improved their bottom line, increasing profits or reversing losses presented in 2021 (see table). On the other hand, the majority were also operating at the end of 2024 with worse gross margins than three years earlier. That is, the profit for each item sold, taking into account the selling price and acquisition costs.

Within that margin, companies must cover the rest of their costs: personnel, supplies or financial costs. Greater efficiency in these expenses, as well as possible windfall revenue, can explain why a company improves its net earnings but worsens its margins.

“Between 2021 and 2024 we experienced one of the most complex periods for the food industry,” summarizes César Vargas, general director of business at Pascual. The Burgos manufacturer falls within the average profile of the companies analyzed: it improved its revenues by 28.8% between 2021 and 2024; Last year it made a net profit of one million, when in 2021 the result was negative; and its gross margin worsened by 2.8 points. “We decided not to fully pass on the increased costs to the consumer and as a result the gross margin was affected,” Vargas analyzes.

Of all the companies analyzed, only three improved revenues, profits and margins. Two of these are dairy companies: Corporación Alimentaria Peñasanta (Capsa), owner of Central Lechera Asturiana; and Industrias Lácteas Asturianas (Ilas), formerly Reny Picot and supplier to Mercadona. They are joined by Sovena, an oil group that also supplies Juan Roig’s supermarkets, which in 2021 was at a loss and operated with a negative gross margin.

Capsa attributes the improvement in its numbers to the fact of being “a more diversified company”, with a greater weight in the catering channel and less in the distributor, and after having increased its proposal in milk derivatives compared to liquid milk, increasingly dominated by private labels. In fact, the producers specialized in these brands are those that operated with the lowest gross margin in 2024: Dcoop (4.5% of revenues), Sovena (7.7%), Acesur (9.5%), Incarlopsa (22.3%), Ilas (23.7%), Jealsa (24.4%) and Profand (30.7%). Only Deoleo is among them, with a gross margin of 17% last year. The four oil groups analyzed, in fact, are in last place in terms of margins, after a period marked by historically low harvests and skyrocketing prices.

«They have been complicated years», recognizes the president of Dcoop, Antonio Luque. “Despite this, consumer response has been better than we all imagined and has delivered industry-wide savings on furniture. Operating costs have worsened, but we have persisted.”

But if companies specializing in white label are those with the lowest margins, producers who compete with their own brands are those who have eroded them the most in recent years. Nestlé tops the ranking, with a reduction of more than 11 points, followed by Deoleo (-9.8), Danone (-8.5) and Campofrío (-6). The latter is one of the few that recorded losses in 2024, and which also worsens the results of 2021. The meat producer highlights, in addition to cost inflation, the adjustments made to its perimeter, with divestments in the United States and Italy that caused accounting write-downs.

Competition with private label is, in fact, one of the great challenges that these producers have had to face, as César Vargas, of Pascual, recognizes, together with “cost pressure and the transformation of consumption channels”.

Progressive stabilization

The trend in 2024 and 2025 is towards stabilized inflation and a gradual recovery in sales profitability. “With the progressive containment of costs, the situation has normalized and little by little the companies have recovered part of the profitability lost in that period,” analyzes the general director of the association of producers and distributors Aecoc, José María Bonmatí. This indicates that, according to an internal prospective study, 52% of companies now prioritize volume growth over margin improvement, “in an effort to gain market share and improve their positioning in an extremely competitive industry.”

This explains that, despite the improvement in profits, gross margins remain lower than those of 2021. “This is possible by implementing measures of low prices or discounts on some products. The mass consumption sector bases its business model on large volumes of sales and economies of scale,” recalls Bonmatí, who assumes that sales in 2025 will improve compared to those of 2024, although he rejects that we are in a context of a general increase in food prices.

Capsa shares the good prospects and aims for an “improvement in indicators, as a consequence of the good performance of all companies”. “2025 shows a positive evolution. The moderation of inflation and the recovery of consumption favor a more stable environment,” says César Vargas, of Pascual.